TPD and super insurance claims pay a lump sum to people permanently unable to work due to illness or injury. Most Australians already hold this cover automatically through their superannuation fund, often without realising it sits there alongside their retirement savings.

Insurers assess claims against specific policy definitions, and even small differences in wording can influence the outcome. vbrLawyers handles TPD and super insurance claims involving different illnesses, injuries, and disabling conditions.

In this article, we will cover how TPD and income protection insurance work, what conditions qualify, and what the claims process involves. We will also discuss death benefits, terminal illness cover, and pre-existing condition exclusions.

What Are TPD and Super Insurance Claims?

TPD and super insurance claims are financial benefits paid to people who can no longer work permanently due to illness or injury. It pays out as a lump sum, entirely separate from the account balance, so it does not draw down retirement savings.

Superannuation funds in Australia, including Australian Super, REST, and Hostplus, automatically include this cover for members, though policy terms vary between funds. The claim is not fault-based either, so a workplace accident, a car crash, or a chronic medical diagnosis each qualifies on equal footing.

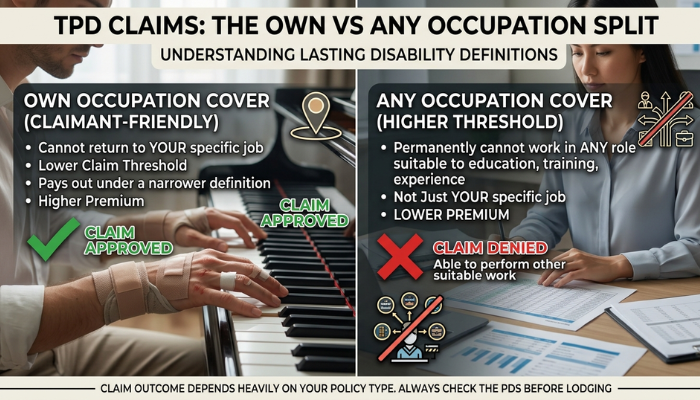

TPD Claims: The Own vs Any Occupation Split

Your claim outcome depends heavily on which type of TPD cover sits inside your policy. In this case, own occupation cover applies when a person can no longer return to the specific job they held before the disability. It carries a higher premium, particularly because it pays out under a narrower and more claimant-friendly definition of a lasting disability claim.

On the other hand, any occupation cover applies when a person permanently cannot work in any role suited to their education, training, or experience. This sets a noticeably higher threshold to satisfy.

The insurance policy wording determines which one applies to you, so you should check the product disclosure statement before lodging anything.

Conditions That May Qualify for a TPD Claim

A lot of people assume TPD is only for physical injuries. In general, conditions including spinal injuries, cancer, heart disease, severe anxiety, PTSD, and depression can all qualify, provided they permanently prevent the person from working.

Treating doctors play a central role here, as the insurer requires medically certified reports confirming these three things:

- The diagnosis

- The functional limitations

- The permanence of the condition

The threshold is permanent incapacity. From our experience working with these claims, medical reports need to reflect no reasonable prospect of recovery, rather than just a current inability to work due to the condition.

Income Protection, Death Benefits, and Terminal Illness

TPD is not the only insurance benefit sitting inside a super fund. In fact, most of them bundle at least three separate cover types into a single policy, and claimants regularly hold eligibility across more than one.

Each benefit type carries its own eligibility criteria, payout structure, and claims process. Here are the details.

How Income Protection Insurance Works

Unlike TPD, income protection insurance does not require a permanent disability to qualify. It covers temporary incapacity and pays out when a person is temporarily unable to work due to illness or injury, providing a regular income.

This is how the main features of income protection cover break down:

- Payment Amount: Income protection payments replace 75-90% of pre-disability earnings, paid monthly to cover lost income during recovery.

- Benefit Period: The cover commonly runs from 2-5 years (up to a certain age), depending on the income protection policy terms chosen at the time.

- Waiting Period: A waiting period of 14 days to 2 years applies before income protection benefits begin. So early lodgement of income protection claims is worth prioritising.

- Temporary vs Permanent: Income protection cover applies to temporary incapacity specifically, which separates it structurally from a TPD claim.

These figures vary between insurers, so checking the income protection policy directly gives the clearest picture of what applies.

Death Benefits and Terminal Illness Claims

Most people set up their super and never look at the insurance cover sitting inside it. Death benefits and terminal illness cover are two types worth knowing about.

A death benefit pays a lump sum payout to a nominated beneficiary when the insured person passes away, sitting entirely separate from the super account balance. Meanwhile, terminal illness claims allow early access to that same benefit when a person receives a terminal diagnosis. This way, families are not left waiting for a payout.

Most super funds require treating doctors to provide medically certified reports confirming the diagnosis before releasing the benefit.

Important Note: Exact life expectancy thresholds vary by fund and need verification against the relevant product disclosure statement before lodging.

Lodging a Claim: What the Process Looks Like

Each stage of the TPD claim process has its own requirements, and missing one can slow the whole thing down. The process starts with contacting the super fund directly to request claim documents, and from there, each step builds on the last.

Below are the main stages involved in lodging an insurance claim:

- Request Claim Documents: Contact the super fund to obtain the correct forms, the insurance policy details, and the product disclosure statement before filling anything in.

- Gather Medical Evidence: After that, collect reports from treating doctors and specialists. They should be able to confirm the diagnosis, the functional limitations, and why the person remains unable to work due to the condition.

- Complete the Application: Fill out all forms accurately next. The form will cover employment history, education, qualifications, and how the permanent disability affects daily function.

- Submit Supporting Documents: Finally, attach medical reports, employer letters, and any other claims-paid documentation the insurer requests as part of the assessment.

After completing everything, the insurer reviews all evidence and, in some cases, arranges an independent medical examination before delivering the insurer’s decision. Strict time limits apply at this stage, so responding to any requests straight away keeps the process moving.

During the process, a claims consultant or financial adviser can assist with preparing the submission. For complex cases involving multiple conditions or important details that the claimant may overlook, we suggest reaching for professional help.

Pre-Existing Conditions and Policy Exclusions

Pre-existing conditions are one of the most common reasons insurers push back on a TPD claim. It generally refers to any illness or injury diagnosed or showing symptoms before the insurance policy commenced. Many policies exclude these conditions outright, meaning the insurer will not pay a TPD benefit for a condition that predates the cover.

That said, exclusions vary widely between insurers. Some conditions only face partial exclusions under a superannuation policy, so reading the fine print of the product disclosure statement confirms exactly what applies.

Medical history plays a significant role here, too. Insurers assess it during underwriting and can apply variable premiums or variable age-stepped premiums based on disclosed conditions.

Multiple Claims and Insurance Entitlements

If you have held more than one super fund, you may have active TPD cover under more than one policy. A person with two or more accounts can lodge multiple claims independently, with each insurer assessing their own policy separately. This is particularly true for those with old or inactive super accounts that they stopped contributing to years ago.

Old accounts, in a lot of cases, still carry valid cover and insurance entitlements worth claiming. Moreover, the balance in those accounts does not need to be large for the benefits to apply. That is why checking every account before lodging is a practical first step.

Other claims, including workers’ compensation, do not automatically disqualify a claim either, though the insurer will factor them into the overall assessment.

Before You Start Your Claim

TPD and super insurance claims cover far more ground than most people initially expect. These policies may provide access to permanent disability cover, income protection payments, death benefits, or terminal illness claims. Each has its own eligibility requirements and assessment process.

Before lodging anything, checking every super account for active cover is a practical first step. Reviewing the product disclosure statement for each policy also clarifies what pre-existing condition exclusions apply. That way, there will be no surprises once the insurer’s assessment begins.

The team at vbrLawyers handles TPD and super insurance claims for Queensland residents across a wide range of medical conditions. Get in touch with our team for information on how the claims process works in your circumstances.